Explore Dallas' evolving grocery landscape with analyst-backed data and exclusive insights from our on-the-ground research team.

Press play to hear exclusive insights about the Dallas grocery market

For developers, landlords, and investors, DFW is a case study in how grocery-anchored retail drives market stability. With record occupancy and demand spilling into suburban corridors, grocery banners are not just tenants here — they are the anchors that define entire trade areas.

Let's dive into the insights...

The full Dallas report goes deeper — block-by-block analysis of store performance, banner expansion tracking, demographic overlays, and detailed competitive benchmarks. Whether you're a grocer, developer, investor, or supplier, this data is designed to give you an edge.

The Dallas–Fort Worth metroplex is the 4th largest U.S. metro by GDP ($613 billion), home to 19 Fortune 500 headquarters and a workforce fueled by technology, healthcare, education, and aerospace. That economic strength translates into a fiercely competitive grocery environment:

Walmart + Kroger control roughly a third of grocery share.

Tom Thumb (Safeway) + Albertsons together hold ~10%.

H-E-B surged from just 1.3% share four years ago to more than 7% today — with 21 stores open and as many as 32 more in planning stages.

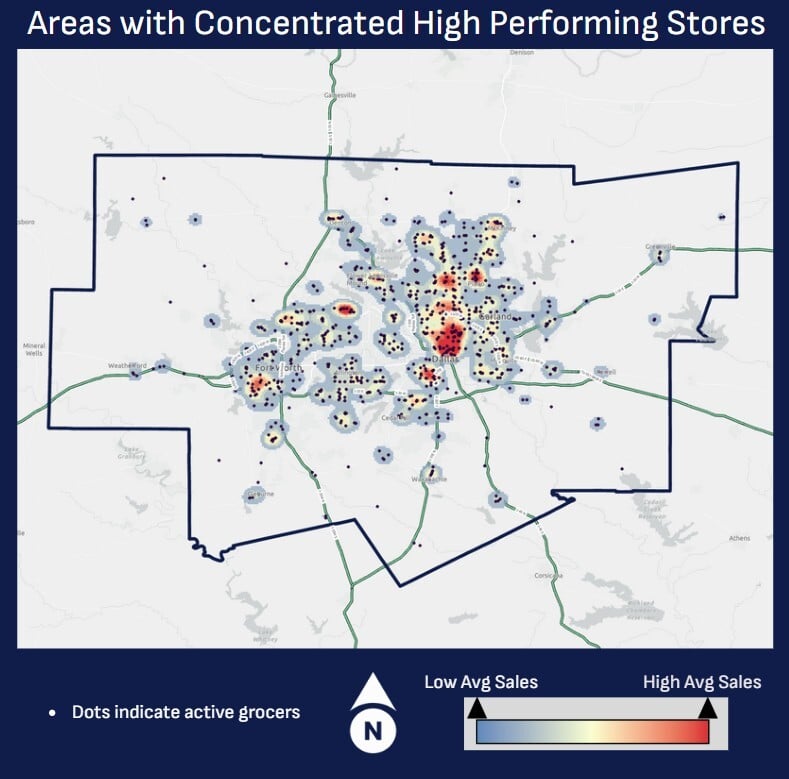

High-performing grocery clusters stretch across the metro:

Nearly half of all retail space delivered in 2024 was grocery-anchored — about 696,000 sq ft — and occupancy rates hit 96.4%. With more than 7 million sq ft of retail construction underway in DFW, grocers remain the top driver of new development.

H-E-B's Prosper store, which opened this month (August 2025), spans 133,000 sq ft and includes a BBQ restaurant, pharmacy drive-up, curbside pickup, fuel station, and cooking demos. The company is eyeing Dallas proper with new land purchases — marking a shift from its suburban strategy.

Whole Foods is expanding in Frisco and McKinney, offering local vendor products and community engagement programs. Specialty grocers like Eataly have faced criticism for steep prices in Dallas, highlighting the divide between premium and value-focused chains.

Kroger continues to invest in multicultural offerings and digital fulfillment but has also begun closing underperforming stores — including one in McKinney — while upgrading others with fresh produce and pharmacy offerings.

While protein costs surged nationally by 9%+ in 2024, Dallas consumers have seen steadier grocery pricing compared to other metros — an advantage in a market where affordability is as critical as quality.

Our on-the-ground analysis has identified the highest concentrations of high-performing grocery stores across the Dallas metro area:

Ready to navigate the complexities and capitalize on the opportunities within the Texas grocery market and so many others across the US? Choose the option that best fits your needs:

Want the full picture? Download the complete Dallas Grocery Market Insights Report for banner growth projections, store-level data, and neighborhood-specific performance analysis.